The Quick Start Guide to Building a Small & Local Business

Whether starting a brick-and-mortar storefront, an online business, or a combination of both, getting a business off the ground can be challenging.

Yet, Americans are starting small businesses faster than ever before. In 2021, 5.4 million people applied to start a business—up 53% from 2019. According to Axios, “the small business boom of 2020 comes after one of the least entrepreneurial decades in U.S. history, the 2010s.”

If you’re part of this new generation of business owners and small business pioneers, we want to help you get up and running faster and more successfully by providing you with a comprehensive guide on what it takes to get a small or local business off the ground and running. Keep reading to learn:

- How to create a solid business plan that will set you up for long-term success

- What’s required for legal and tax compliance

- How to finance, manage, and market your business

Why start a small and local business?

The news headlines may be filled with the triumphs of big businesses like Google, Apple, or GE, but the truth is small businesses are the lifeblood of the American economy, driving innovation and competitiveness across all sectors of industry. Currently, small businesses account for about 44% of the economic activity in the United States and make up 99.9% of all U.S. businesses.

There many reasons to start a small business—some people want to build something from the ground up, others are looking for more flexibility and control, and others “fall into” starting their own business after being laid off. No matter what’s motivating you to start your business, before you dive in, make sure to consider both the risks and the rewards.

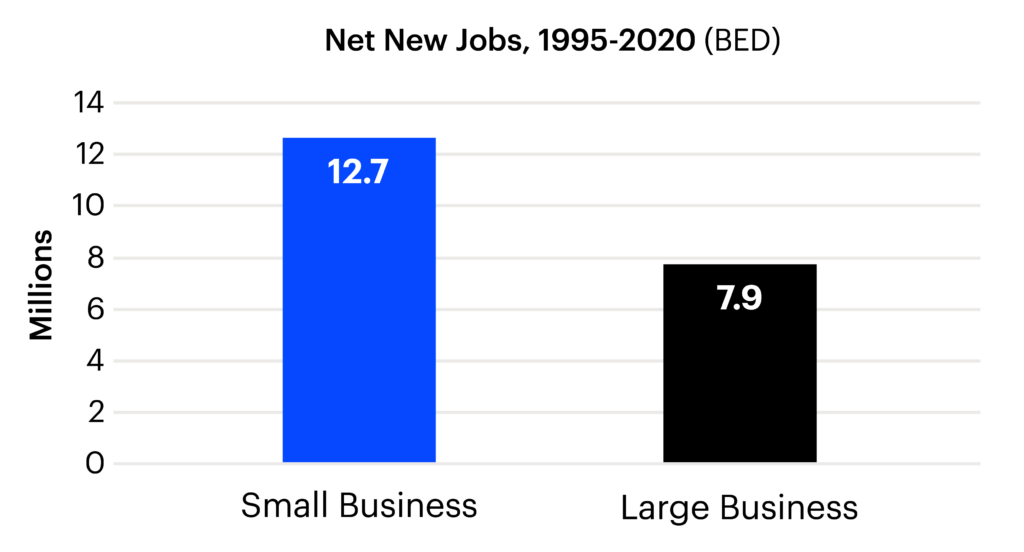

Jobs created by small businesses vs. big businesses

Source: Small Business Association

Benefits of small and local businesses

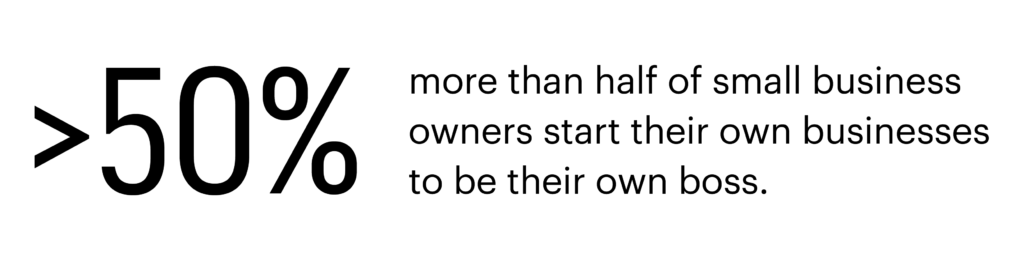

While money can be a key motivator for starting a business—and 65% of small business owners say they are profitable—it is often not the key driver or even the biggest benefit for most small and local business owners. According to one study, more than half of small business owners start their own businesses to be their own bosses. Only 8% of respondents said money was the main motivator.

Greater flexibility, freedom, and control are often other big motivators for owning a small business. But perhaps the biggest benefit is that most business owners say they are simply happier running their own business, with 75% saying they are very to somewhat happy.

Challenges and risks to consider

While owning your own business can be highly rewarding, it’s not without risk. According to the Small Business Administration, approximately 33% of small businesses fail in the first two years, 50% fail within five years, and just 33% make it to 10 years or beyond. A tough economic climate can also make it difficult for small businesses to thrive. For instance, 88% of small business owners say today’s high inflation is impacting their business.

Other challenges that can impact a business’ survival include not planning effectively, poor marketing, hiring challenges, and financing hurdles. In the following sections, we’ll look at each of these challenges and offer you guidance on how to avoid these risks so you can set your business up for the greatest success.

Creating a business plan

A business plan is essential to every business—both large and small. It defines your business objectives and how you will achieve those objectives. A business plan isn’t only essential to getting funding (every funder will want to see your business plan), it also creates a roadmap for how you will run, manage, and market your business.

According to Liveplan, here’s how most small businesses use a business plan:

- 39% reposition and find new strategies

- 36% revisit financials and check the viability

- 25% to find customers

- 70% to create business

- 42% to attract investors

Defining your business goals and objectives

The first step of your business plan is understanding your goals and objectives. These are often split into long-term and short-term goals you hope to achieve. For example, a short-term goal might be to increase your quarterly revenue by 10%, hire three new employees in the next year, or increase the number of customers you have by 20%.

Longer-term goals are more of a vision of where you want to be in five or ten years. These goals will be bigger and take longer to reach. Maybe you want to open five new locations for your business in five years or be doing a million or more in revenue in ten years. Or, maybe your goals are less monetary and more visionary, such as having your business running smoothly enough that you have more freedom and flexibility to spend more time with your family, travel, etc.

Whatever the goals are for your business, once you’ve defined them, you’ll want to map out how to achieve them. One way to do this is using the SMART goals strategy:

- Specific

- Measurable

- Achievable

- Realistic

- Time-bound

Following this framework makes it easier to ensure that you have a very clear plan as to what your goals are, how, and when you’ll achieve them—and because they are realistic, you’re more likely to succeed.

Identifying your target market

In order to drive customers to your business, you need to first understand who the best-fit customer is for your business. You can do this by creating a buyer persona for your ideal customer. A well-defined buyer persona typically includes the following information:

- Demographics: Age, income, education level, and marital status

- Psychographics: Values, lifestyle, hobbies, and morals/beliefs

- Pain points: Problems they have that your business can solve

- Channel preferences: Digital and physical channels to use and interact with your business

Outlining your marketing and sales strategy

Whatever your goals are—whether it’s increasing revenue, customers, or brand awareness—you’re going to need a marketing and sales strategy to help you achieve them. Your marketing strategy will focus on building brand awareness of your business. This will help you find what’s known as qualified leads—potential customers that are highly likely to purchase your products or services.

Your marketing plan also sets the roadmap for your sales strategy, which will build on your marketing strategy to convert qualified leads into customers.

At a high level, your marketing and sales strategy should outline the following:

- Who is your target audience is

- What your marketing and sales objectives are (you can use SMART goals here)

- How do you plan to reach out to your target audience

- What KPIs are you will use to measure your effectiveness

Developing a financial plan

Another part of your business plan needs to focus on how you will finance your business. This is especially important as you are getting started, as you want to have a clear plan for how to support your business in the early stages when you may not have much revenue coming in.

While some businesses are bootstrapped, which means the funding is provided by the owner, for many small and local businesses, there are a lot of upfront costs, such as buying inventory, leasing a business office, and hiring staff that requires additional financing assistance to cover.

Your financial plan should outline what these expenses are, what your projected revenue is for the first year or more, and how you will cover the costs, such as getting a loan from a bank, small business grants, investors, or family and friends.

A solid financial plan allows you to have a realistic understanding of what it will cost to run your business and ensure that you have the means to do so.

Choosing a business structure

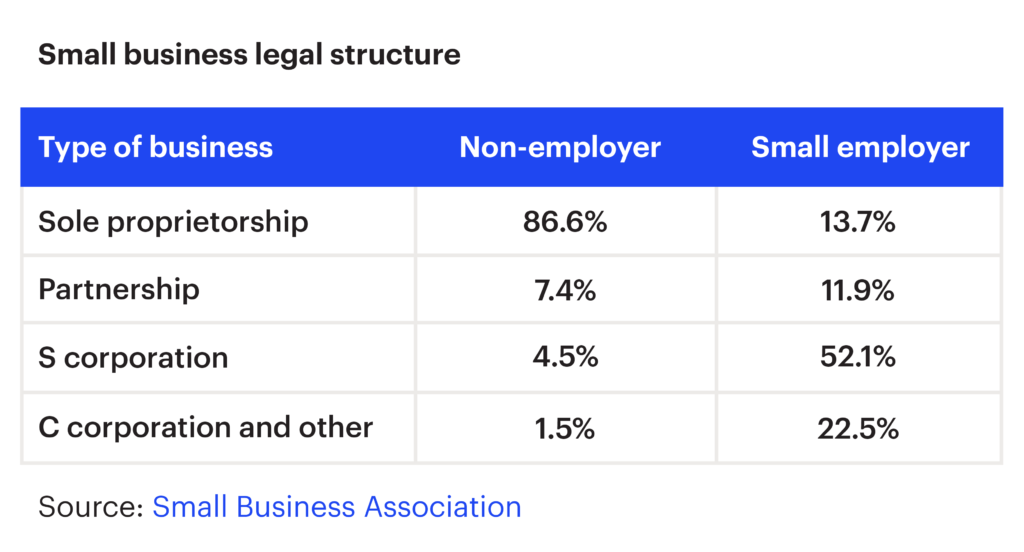

The last part of your business plan is determining what type of business structure you want to use. There are a couple of different ways you can structure your business. Each one has different advantages and can have different impacts on your tax payments and personal liability.

- Sole proprietorship: This is the simplest business structure as it’s set up under your personal income on your tax return. Registration is simple or often not even required. However, sole proprietorships put you, your credit, and your personal assets at risk in the case that you default on a loan or get a lawsuit. While sole proprietorship can be convenient when you’re just getting started, many small business owners move away from this business structure as their business grows.

- Partnership: A general partnership is best described as a sole proprietorship for a business with multiple owners. You avoid double taxation and can easily register your business, but you still assume personal liability.

- Limited liability company (LLC): Creating an LLC will require some paperwork and registering your business. However, you do receive the benefit of protection from personal liability since this type of business structure makes your company an entity that is separate from you. Depending on elections made by the LLC and the number of members, an LLC can be taxed as a corporation, partnership, or as part of the owner’s tax return.

- S corporation: The most common corporate entity, S corps provides a higher level of personal liability protection than LLCs while still only being taxed once. This structure also allows you to take on more shareholders and investors. It is the most common business structure for small businesses with employees.

Registering your business

Now that you’ve got a business plan in place, you’re ready to get your business registered. Whether your business operates in a retail space or at home, it’s important to register your business. The main advantage of registering your business is that it can shield you from potential legal and financial liabilities. However, registering can also give you more access to business loans and grants.

You will need to register your business at the federal and state level. Here’s how:

- Federal registration: You will need to apply for a federal tax identification number known as an employer identification number (EIN) on this IRS page by clicking “Apply Online Now.” If you selected sole proprietorship as your business structure, you do not need to register for an EIN. However, if your business is structured as an S corp, you will need to also complete Form 2553 and submit it to the IRS.

- State registration: State registration varies by type of business structure. In some states, business owners, including sole proprietors, must apply for a state tax ID number separate from their federal tax ID number. If you are planning to operate in multiple states—this includes if you will have employees in the state or plan to earn a large amount of revenue in a state—you must register in each of these states and have an eligible registered agent within each one.

- LLC: Owners of LLCs must submit a legal document called the Articles of Organization to register a company. Known as the Articles of Formation in some states, this becomes the official documentation of your company name, office address, registered agent, and even your purpose. It can cost anywhere from $50 to $500 to submit this paperwork, as state fees vary widely.

- S corps: Owners of S corps must submit the Articles of Incorporation, which is similar to the paperwork for LLCs but adds information about who is on your board of directors and how many shares of stock you’re giving out. This paperwork can cost around $100 to $250.

Choosing a business name

As part of registering your business, you will also need to select a business name. This can match your legal name, such as John Smith, Inc., or it can be an entirely different name, like Perfect Smile Orthodontics. Additionally, you can choose to also register your business name through the U.S. Patent and Trademark Office to give you extra security for your brand.

Additionally, you’ll want to create a brand image around your business name to gain credibility under that identity. This includes setting up banking transactions with vendors and customers that include your business name. A separate business bank account will also help legitimize your business should IRS question its classification and will help you keep your business and personal finances separate.

Filing for a business license or permit

While you don’t need to submit any official documentation to start doing business in your city or county, you may need to apply for and maintain a business license or permit to operate in some areas. Your local government websites are your best resource here since laws vary based on your zip code, industry, and type of business structure. You may need to pay a couple of hundred dollars in fees to apply for a license or permit and up to $100 for renewal each year.

Here are a few other tips that could help you through the permitting process:

- Search your state business hub: Most state websites feature a business licensing and registration information page, making it easy to research requirements and gather the required forms.

- Check for prerequisites: Make sure you’re following the right steps in the right order.

- Read the fine print: Read all the instructions on the website and forms before you fill out any form. Some requirements are not very clear on the forms themselves, but you can usually find instructions somewhere on the site.

Registering for taxes

As discussed above, registering for tax purposes generally requires applying for a federal EIN or other tax identification unless you are filing as a sole proprietorship. You may also need other tax identification through your state’s revenue department, and unless you’re operating as a sole proprietor, your registration process will require you to submit the contact details for a registered agent.

You also need to be aware of periodic tax payments or other tax liabilities your business may be required to file. These might include:

- State income and franchise taxes: Some states have a flat franchise tax, be sure you know whether this applies to states your business will be operating in.

- Sales and use tax: Check state revenue department websites for sales and use tax thresholds and requirements in any state where you have taxable sales. If your business is a wholesale distributor, you may need to apply for a reseller’s certificate.

- Employment taxes: You will need to register for state payroll taxes in states where you have employees. You may also have to register with the state labor department for workers’ compensation and unemployment insurance.

- Local taxes: Your business may also have to be registered at the county and municipal levels.

Protecting your business with insurance

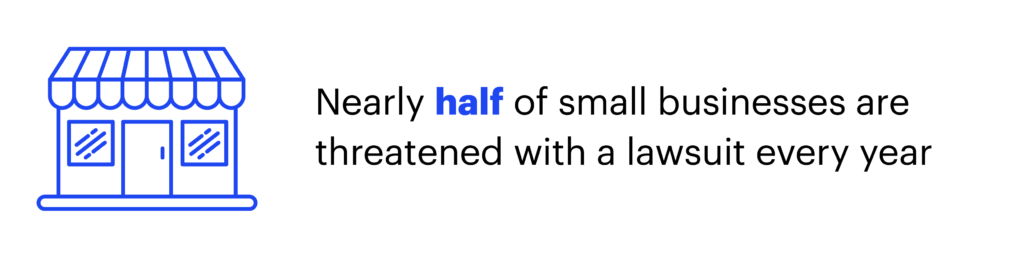

Nearly half of small businesses are threatened with a lawsuit every year.

For this reason alone, it’s important to carry business insurance. However, business insurance can also protect against accidents, natural disasters, and other unexpected events.

There are a number of different types of insurance you can purchase for varying amounts of coverage. Here’s what you should consider:

Type of insurance you need

A BOP provides basic coverage and is adequate for many small businesses as it protects your building and contents as well as provides protection due to a defective product or service mistake that causes harm to others. However, there are a number of other types of insurance your business might also need, including workers’ compensation, commercial property, professional liability, cyber liability, and commercial auto insurance. Consider what type of business you operate and which types of insurance are necessary to cover your business.

The type of business you operate

The size of your business and whether your business has clients that regularly visit your place of business can impact the cost of insurance and the type of insurance. Even if you’re running your business out of your home, such as a daycare, hair salon, or therapy practice, adding an endorsement to your homeowners’ policy is likely not enough protection, and you’ll need to procure a separate commercial insurance policy to ensure proper coverage.

Your level of risk

Consider the potential dangers to your business, such as natural disasters or workplace accidents. Your business’s primary risks would inform your policy purchases.

Find the best price

It’s worth it to compare prices, terms, and benefits from multiple offers, as insurance rates can vary by provider. The Small Business Administration (SBA) can also provide guidance to help you determine how much you should spend on policies to protect your specific type and size of business.

Assess your coverage annually

Your business is likely to grow and expand, which can mean your liabilities and risks evolve as well, so it’s good practice to assess annually whether you have adequate coverage for all aspects of your business.

Remember, insurance is about protecting you, your employees, your business, and your customers. It’s rough out there:

- 90% of all businesses experience a lawsuit at some point in their lifespan

- 43% of all small businesses are threatened with a lawsuit every year

- 43% of all cyberattacks target small businesses

Hiring and managing employees

With the current labor shortages, hiring has become even more challenging for small businesses. Currently, more than half of small business owners report that recruiting and retention of employees is one of their top three challenges. Moreover, small businesses have been among the hardest hit during this staffing shortage, as they don’t have the resources or reputation to keep up with larger companies that are hiring.

Despite these challenges, there are a lot of things small businesses can do to overcome challenges with finding and retaining the right employees.

Finding the right employees for your business

With the cost of replacing an employee ranging from one-half to two times the employee’s annual salary, it’s crucial for small businesses to find the right hires the first time around. These tips will help you better align what type of person and skills you need to improve your chances of making a good hire:

Make sure you need to hire

Before you begin the hiring process, make sure you have thought carefully about whether you need permanent help or temporary help. Also, figure out how many hours of work you have for an employee each week. Finally, consider whether technology and automation could do some or all of the job.

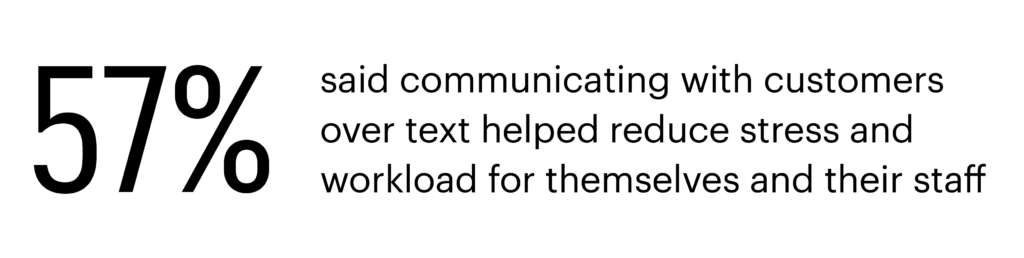

In a recent survey, 44% of small and local business owners say they have opted for technological solutions as an alternative to hiring. Over half (57%) said communicating with customers over text helped reduce stress and workload for themselves and their staff.

Map out a career path

A lack of career development opportunities and room for career growth is the top reason employees quit, according to McKinsey. Even if the job you’re hiring for is a minimum-wage position, you’ll want to think about how that person might be able to move up in your company as you grow. If it’s a higher-level position, such as a manager, it’s even more important to consider how you can continue to offer growth potential in the company.

Provide the right compensation

This requirement can be especially challenging for small businesses that may have tight budgets. But in today’s tight labor market, you simply must be competitive to attract employees. Inadequate total compensation was the second most common reason (36%) employees quit.

If you can’t offer a competitive salary, consider what other perks you can provide. Sometimes as a small business, you can offer benefits that other large employers can’t, such as more flexibility in an employee’s work schedule, the ability to work remotely or bring a pet to work, or a faster path to career growth.

Creating job descriptions and hiring process

As a small business owner, you’ll likely need to manage the entire hiring process yourself. It might feel a little overwhelming, but if you take it step-by-step, the process can go smoothly.

Here are some of the critical tasks you need to do to ensure you find and hire the best employee for the job:

Be clear on the role and responsibilities

Before you even write your job description, start by making a list of the responsibilities the role will involve and what skills are needed. Then, you can effectively translate this into your job description.

Write an effective job description

Your job description should make it clear to any applicants if they are a good fit for the job by clearly mapping out the skillsets required and the types of responsibilities or tasks the employee will need to do. The more detailed you can be, the more likely you are to get applicants who are a good fit.

In addition, finding a good fit cultural-wise is also important. When writing your job description, use a tone that matches the traits you want in your employees and represents the overall culture of your business.

Some highlights your job description should include:

- The job title (preferably one that will come up in a search for relevant jobs)

- A description of day-to-day activities and responsibilities

- An outline of the employee benefits (such as flexibility, discounts for local businesses, or allowances for parking or coffee)

Effectively advertise your job opening

In today’s tight labor market, your job ad needs a lot of visibility. Here are some ideas of where to advertise it.

- Post your job ad online: Start with the best-known websites for job seekers, such as Indeed, Glassdoor, LinkedIn, ZipRecruiter, and Monster.

- Industry-specific website and private online groups: If there is an industry-specific website, consider posting the job ad there. Also, post it in private groups, such as on Facebook or Slack channels that are relevant to your industry and location.

- Local job listing website: If your town has a site, post it there as well.

- Ask for referrals: Current employees can be a great source for referrals, as can other family and friends.

Screen and interview applicants

Rather than spending your time interviewing each applicant, try to narrow it down to the top five or so applicants. Eliminate applicants that might not be a good fit. For example, if an application has a lot of spelling or grammatical mistakes, doesn’t follow instructions, or doesn’t have the prerequisite skills you’re looking for, you may want to skip interviewing them.

Once you’ve narrowed the pool, you’ll want to call in the finalists for an interview. Before you go into the interview, prepare a list of questions you can ask. Be consistent across all interviews, so you’re measuring apples to apples in how applicants respond. Use the interview to determine which applicant has the best skills, personality, and cultural fit for the role and for your business culture overall.

Managing and training your employees

Many employees wind up leaving a new position within the first six months of their employment due to a lack of training. After investing so much in the hiring process, the last thing you want to do is lose employees because you didn’t take the time to onboard and train them properly.

Here are a few tips to help you effectively train and manage your employees:

Clearly communicate job expectations

One of the most important things you can do when training and managing employees is to clearly communicate what is expected of them in their role. This can include specific tasks, goals, and deadlines, as well as any company policies or procedures they need to follow. By setting clear expectations, you can help ensure that your employees understand what they are responsible for and how they are expected to perform.

Provide ongoing training and development opportunities

Provide ongoing training and development opportunities. This can include formal training programs, workshops, and mentoring, as well as opportunities for employees to learn through on-the-job experience. By investing in your employees’ growth and development, you can help ensure that they have the skills and knowledge they need to be successful in their roles.

Create a positive work culture

A positive work culture is essential for employee engagement and motivation. Encourage open communication, show appreciation for a job well done, and provide employee benefits that are relevant to your team. This will help create a more productive and motivated workforce.

Monitor and evaluate performance

Regularly monitoring and evaluating employee performance is an important part of managing employees. By providing regular feedback and coaching, you can help ensure that your employees understand what they are doing well and where they need to improve. This will help you identify and address any issues or concerns and help your employees grow and develop in their roles.

According to BambooHR, employees’ top onboarding preferences include:

Financing your business

Starting a business costs money. Even home-based businesses have a starting cost of between $2,000 to $5,000, and a retail business’s average starting cost is $32,000. If you’re opening a food business, starting costs could be as high as $125,000. The bottom line: you will need some amount of financing to get your business off the ground.

Funding options for small businesses

For nearly a third (28%) of business owners, cash flow is the biggest challenge they face. With major financial institutions approving only 26.9% of small business loans, many business owners have to look elsewhere for funding.

Other funding sources for small businesses include:

- 37% cash

- 13% 401(k) rollovers for business start-ups or 401(k) financing

- 12% line of credit

- 10% family or friends

Despite the low approval rate for loans from major financial institutions, there are other loan opportunities small businesses can pursue. In fact, 43% of small business owners have applied for a loan from a small business lender.

Open a business bank account

Business loans have strict processes for approval, including the existence of a business bank account. Lenders also want solid evidence that you will make timely payments, so you’ll need to provide financial proof that shows responsible recording keeping and gives lenders accurate and organized information to analyze.

Choose the right type of loan

There are several different types of loans you can apply for as a small business, including:

- Term loans

- SBA loans

- Lines of credit

- Equipment loans

- Commercial real estate loans

- Merchant cash advances

Each of these loan types will have different payment terms and advantages and disadvantages. For example, term loans are typically fixed monthly payments, while a line of credit can be based on a variable interest rate and thus, payments may fluctuate based on the current interest rates. SBA loans can be a great choice, but often take months to get approval, whereas if you need cash quickly, a merchant cash advance will give you access to funds quickly but comes with high-interest rates, making it riskier. Be sure you understand the tradeoffs and decide on the type of loan that will be best for your business’s unique circumstances.

Applying for a grant

Grants are different from loans because you don’t need to pay back grants. Most grants for small businesses are from the federal government. However, nonprofits, private corporations, and local governments can also offer grants.

You can start your search for grants that might be a good fit for your business at Grants.gov, a centralized federal website with information on grant opportunities from more than 20 agencies. Keep in mind that those awarding the grants will typically have specific terms for the grant, such as providing research, specific deliverables, or meeting certain KPIs. If you don’t meet these terms, you may be required to pay back the grant.

Crowdfunding and alternative financing options

Alternative funding options for small businesses are growing, and more small business owners are getting creative about how to drum up funding. If you’re looking for a non-traditional path for financing, here are some ideas that might work for you:

- Crowdfunding: With crowdfunding, you need to have a business plan that you can share on a crowdfunding platform. Individuals who like your plan can then choose to donate to your business. If you already have a large audience or following, this can be a successful route to funding. However, it can take a long time to raise enough funds, so it may not be the best option if you’re looking to move quickly.

- Venture capitalists or angel investors: These are companies or individuals who fund startup businesses. The benefit of this type of funding is that you can often get more capital than other funding sources, and there are no interest rates. However, you may be required to give up a percentage of ownership in the company.

- Pitch competitions: Pitch competitions are a great way to gain exposure for your business while also securing financing. The way the competition works is that you propose your business plan to a panel of judges who are also investors. Winners are awarded cash prizes and other support, such as mentorship. Shark Tank is a well-known business pitch competition. The downside of pitch competitions is that the competition can be intense.

Marketing and promoting your business

Marketing is an essential component of running any business. In fact, 50% of businesses view marketing as their main strategy for growth. While many small business owners must wear the marketing hat—at least until their company starts to grow—it can feel overwhelming, and many small business owners aren’t sure where or how to start.

In this section, we’ll lay out a simple path to marketing success for your small or local business.

Developing a marketing plan

Your marketing plan outlines the strategies, tactics, and goals for promoting the business and its products or services. It should include the following:

- Analysis of target market: This includes researching the demographics, needs, and preferences of the target market, as well as identifying the key competitors and their strengths and weaknesses. This information can then be used to identify unique selling points and positioning for the business.

- Set clear and measurable goals: Identify specific objectives, such as increasing brand awareness, driving website traffic, or boosting sales. These goals should be closely tied to the overall business goals and should be specific, measurable, attainable, relevant, and time-bound (SMART).

- Detail-specific strategies and tactics: This includes the channels, such as social media, email marketing, and content marketing, that will be used to reach the target market. It should also include a detailed plan for how your business will measure and evaluate the effectiveness of different strategies, such as tracking website traffic, monitoring social media engagement, and analyzing sales data.

- A detailed budget: Marketing costs money, so you need to outline the costs associated with implementing the strategies and tactics. This includes costs for advertising, public relations, social media, events, and promotions.

Creating a website and online presence

With 70% of consumers learning about a new business online, either through a website or social media, it’s essential your business have a presence online. Here are some tips on how to make sure your business is easily found online.

- Choose a domain name: This is the website address for your business. It should closely match your business name and be easy to remember.

- Create your website: You can choose to use a website builder, such as Wix or Square, or outsource this to a web designer. Website builders offer a range of templates and tools that can be used to create a professional-looking website without the need for extensive technical skills. It’s important to choose a platform that’s easy to use, customizable and can handle business needs. You can learn more about building a small business website in our comprehensive guide—Website 2.0.

- Create content: After your website is created, you can then focus on creating content for the site. This includes creating a homepage, an about page, and product or service pages. It’s also important to make sure that the website is optimized for search engines so that it can be easily found by potential customers. This can be done by including keywords in the website’s content, meta tags, and URLs.

- Use local SEO to help your business get found online: Local SEO uses geographically related keyword searches to help connect local businesses with customers who are looking for products or services your business offers in their local area. With 46% of all searches focused on local information, it’s important to create and optimize your Google My Business profile and your website for mobile so that your business can easily be found in local searches.

- Establish an online presence through social media: Social media is an excellent way to engage with customers, build brand loyalty, and drive traffic to the website. This can include creating a business page on Facebook, Twitter, Instagram, or LinkedIn and regularly sharing updates, promotions, and other content. Determine which social media channels are preferred by your target audience for the greatest success.

- Build your online reputation through reviews: Online reviews can help to build trust and credibility with potential customers. Encourage customers to leave reviews on sites like Google, Yelp, or Facebook. This can be done by providing excellent customer service and making it easy for customers to leave reviews, such as by texting them a link to leave a review.

Networking and building partnerships

Networking and partnerships can be powerful tools for small business marketing. In fact, 95% of professionals think face-to-face communication is vital for long-term business. However, networking can be done in person or online. Trade shows are one way you can network your business. In fact, businesses say about 5-20% of customers are found through tradeshows.

Social media platforms like LinkedIn can also be a valuable networking tool for small business marketing. According to one study, 35% of respondents said that a casual conversation on LinkedIn has led to a new business opportunity.

Business partnerships are another way to market your company and can be especially valuable for small businesses because they can help you develop alliances that can allow you to compete better with big businesses. One of the most common partnerships can be with your vendors or suppliers. Not only do you already have a relationship with these businesses, but you often have aligned interests. An example of a strategic partnership might be if you’re a plumber and you partner with a plumbing supply vendor. You buy your parts from them, which increases their sales, while they refer customers to your business, increasing your sales.

Advertising and public relations

Advertising and public relations are two important strategies that small businesses can use to market their products or services. Both strategies can help to build brand awareness, increase visibility, and drive sales, but they are different in terms of their approach and execution.

Advertising is a paid form of promotion, which can include television, radio, print, and online ads. Advertising can be an effective way to reach a large audience quickly, and it allows small businesses to target specific demographics or geographic areas. But advertising can get expensive quickly, so it’s important to carefully plan and budget your advertising efforts and to ensure that the ads are placed in the most appropriate and effective media outlets.

Public relations (PR), on the other hand, is a form of earned media in which your business leverages relationships with journalists and influencers to gain coverage in the press. Public relations can be an effective way to build credibility and trust with potential customers. In fact, it’s better at building trust and credibility than advertising. According to one study, PR can be 90% more effective than advertising. It can also be a cost-effective way to reach a large audience.

Despite PR’s effectiveness, it can be harder to generate good PR consistently, so a balanced approach between PR and advertising is often a good strategy.

Tips for success as a small business owner

Starting and running your own business does take a lot of effort, but the rewards often outweigh both the work involved and the risks. If you follow the tips in this guide, you’ll be well on your way to success. Remember to:

- Create a detailed business plan

- Determine your target audience

- Develop a sales and marketing strategy

- Plan out how to finance your business

- Hire and retain employees effectively

- Follow all the legal requirements for starting and running a business

With all of these actions taken, your business has a strong foundation on which to grow and succeed.